The Soaring US$!

Charts created using Omega TradeStation 2000i. Chart data supplied by Dial Data

The headlined blared – “Global rate-cutting frenzy could freeze U.S. economic recovery” (Globe and Mail, Report on Business, February 4, 2015). This seemed to fly in the face of an FOMC that the US economy “has been expanding at a solid pace”. The FOMC cited an improved labour market, modestly rising household spending and lower energy prices boosting household purchasing power. The FOMC also cited that business investment was advancing. If there was a concern it was that inflation had fallen below the “Committee’s longer-run objective” and they also thought that inflation could fall further in the near term but they expected inflation to rise gradually towards its 2% objectives.

While many are expecting the Fed to hike interest rates sometime later in 2015, a careful read of the FOMC’s statement reveals that they never actually say that. All they say is that they “will assess progress….toward its objectives of maximum employment and 2% inflation”. Yellen has constantly used the word “patience” when it comes to rate hikes. For the Fed though the growing trouble is will they meet their objectives? While headline unemployment continues to inch lower inflation is moving lower as well. The risk is not inflation but deflation.

Deflation is gripping the Euro zone and Japan and could now grip the US as well. The year-over-year headline inflation rate for the US was a paltry 0.8% in 2014. In the Euro zone, inflation has turned negative and Germany has recorded deflation for the first time since 2009. The ECB’s €1.1 trillion QE program is an attempt to revive the Euro zones sagging economy and hopefully stave off full-blown deflation. The Euro had been falling since March 2014 when it peaked at 1.3950. Following the ECB QE announcement the Euro fell further to a low of 1.1230.

Over the past several months not only has the Euro been falling against the US$ but it seems all the other currencies have been falling as well. Currencies for the most part peaked in March 2014. Since then the Euro is down about 18%, the Japanese Yen is down roughly 13%, the British Pound is off 11%, the Swiss Franc (who unpegged from the Euro) is down just over 5% and the Cdn$ is off over 15%. And that’s the major currencies. Numerous emerging market currencies have fallen even further. The Russian Ruble is down 52% since June 2014.

One currency is not mentioned. Gold. Many would argue that gold is not a currency. However, if gold is not a currency then why do the central banks of the world still hold roughly 32,000 metric tonnes of gold in their monetary reserves? And why are so many countries, particularly Russia and China, adding to their gold reserves? Since gold bottomed in November 2014 it is up just under 11% against the US$ although it is down from March 2014.

The strength of the US$ caught a lot of market participants by surprise. There were many who thought that following QE1, 2 and 3 that the US would descend into hyperinflation and that would result in the collapse of the US$. It did not happen. The rising US$ is actually causing deflation. First comes the rising currency signaling the onset of deflation then comes the falling currency signifying potential hyperinflation. For months the Euro was rising. Until March 2014 that is. The rising Euro may have been signaling the coming deflationary drop.

So why is a rising currency deflationary? For the US, it has made imports cheaper (falling prices) so consumers could benefit. On the other hand, US exports could become more expensive meaning they the US could sell less abroad. Note that the most recent US trade deficit widened unexpectedly to $46.6 billion, a 17% rise. It was the largest monthly rise on record and the widest since November 2012.

The net result overall is that while imports are cheaper the drop in exports could lead to job losses and workers having less to spend. US multinational corporations are also hurting as upwards of 60% of their earnings are from outside the US. With those currencies falling against the US$ the large multinational corporations are starting to report declining earnings (deflationary).

A strong US$ can also hurt those with debt as the value of the debt rises relative to the falling prices and incomes. Median income in the US today is $28,601 vs. $28,176 in 2000 (adjusted for inflation). Incomes are stagnant but debt has gone up. To put that in perspective the median cost of a new home today is $281,593 and in 2000, it was $169,738. Moreover, today’s price is after a roughly 20-30% drop in housing prices since 2007.

Despite three rounds of QE, the US economy may be performing somewhat better than other economies but overall the US economy continues to perform well below its long-term potential. The Q4 GDP came in at 2.6% below the expected 3.2% and below Q3’s 5%. For 2014, US GDP is expected to come in at 2.3%.

Three rounds of QE has exploded the Fed’s balance sheet. Since August 2007, the Fed’s balance sheet has grown from $869 billion to $4.5 trillion today. The US monetary base has exploded from $950 billion in Q3 2008 to $4.1 trillion today a gain of over 330%. But has money supply grown? Not by much. M1 (currency in circulation and demand deposits) is up 98% in the same time-period, M2 (M1 plus savings and time deposits) is up 48% and M3* (M2 plus large time deposits of financial institutions) is up less than 11%. The anaemic growth of M2 and M3 is a prime reason why there is no inflation and why the economy is not growing to its potential. During the 1990’s M3 was the fastest growing component of the M’s. In the latter part of 2009 and early 2010 M3 actually experienced negative growth.

* M3 is no longer tracked by the Federal Reserve. Shadow Stats www.shadowstats.com does track M3.

Loan growth in the US has not exactly been a “barnburner”. Total loans have gone from $52 trillion in Q3 2008 to $57.9 trillion today a gain of only 11%. The prime reason for the growth has not been the consumer or the corporations but government. Government debt held by the public has exploded by 120%; mortgage debt has fallen by 12% although consumer credit card debt has gone up 22%. Quite simply all that money that the Fed used to buy mortgage backed securities and government debt from the banking system has not, for the most part, found its way into the economy. If it had, mortgage debt would be a lot higher and M3 would be a lot higher.

where has all the money gone? Speculation primarily. The stock market as measured by the S&P 500 has gone up almost 200% since the depths of the 2008 financial crash. As if the measurement of an economy’s strength should be measured primarily by a rising stock market even as the rest of the economy has demonstrated at best anaemic growth. US GDP is up about 18% since Q3 2008. Considering the US population has grown 5%, GDP growth is not overly impressive. That has raised the Government debt to GDP ratio to 104% in the past few years. Total debt to GDP is around 340%. That is not bad when compared to Japan that has a total debt to GDP ratio of over 650%.

The US’s QE 1, 2 and 3 plus QE in Japan put trillions into the banking system. Given sluggish loan growth in the US it did not appear to go into loans to consumers and corporations. The stock market was a major beneficiary but one of the largest beneficiaries was emerging markets. Huge amounts apparently went into what is known as carry trades. It is estimated that upwards of $11 trillion went into emerging market debt. Two thirds of that is estimated to have been in US$. But what happens when the currency borrowed strengthens and the currency that enables to pay your principal and interest weakens? The potential result is the destabilizing of foreign markets as the potential for defaults rise.

With money flowing primarily into the stock market and emerging market debt and not so much into the domestic market it is little wonder that inflation has not become a problem. Instead it is the growing threat of deflation that is the problem particularly if the emerging market debt were to default. The rising US$ has not yet resulted in defaults but the potential is there.

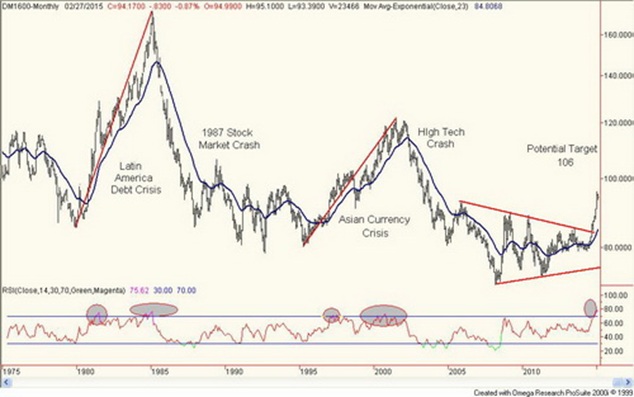

There has been two other periods where the US$ was rising sharply. Former Fed Chairman Paul Volker triggered the rise of the US$ from 1980 to 1985 when the Fed hiked interest rates to 20% in late 1979. The US$ Index rose from 85.45 to 172.77 during that period, a gain of 102%. The Latin American debt crisis exploded during that period. Latin America had borrowed huge sums of money in the 1970’s primarily in US$. Latin American external debt soared from $75 billion in 1975 to $315 billion by 1983.

The Plaza Accord of September 1985 was designed to depreciate the US$ as the sharply rising US$ was causing considerable problems for US exports (sound familiar). The subsequent depreciating of the US$ sparked a stock market rally and helped push up interest rates and inflation in the US. Two years later the stock market crash of 1987 was sparked in part by the collapsing US$.

The second huge rise in the US$ Index occurred between 1995 and 2000. The US$ Index rose from 80.14 to 121.29 a gain of 51%. Japan and the US had agreed to raise the value of the US$ vis-à-vis the Japanese Yen as Japan was experiencing export woes because of the high value of the Yen. So what happened. The Japan/US accord set in motion what became known as the Japanese Yen carry trade, which resulted in huge flows into the US markets pushing bond yields lower and resulting in a soaring stock market. As with the Latin American countries of the 1970’s the Asian Tigers (Thailand, Indonesia, South Korea amongst others) had seen their foreign debt to GDP ratios explode during the early part of the 1990’s as they took advantage of the weak US$ borrowing primarily in US$ to finance their boom. Their currencies were also largely tied to the US$. As the US$ rose they found themselves unable to service their huge foreign debt.

The crisis was twofold. The first phase occurred in 1997 and the second phase occurred in 1998 when Russia defaulted sparking the near collapse of Long Term Capital Management (LTCM) a huge hedge fund that almost brought down the financial system in the fall of 1998. The large money center banks and the Fed saved LTCM as the Fed flooded the financial system with liquidity and dropped interest rates. Two years later the high tech/internet crash got underway as the bubble created in part by the Japanese carry trade collapsed. The US$ Index also collapsed as the US fell into recession. The events of 9/11 also helped crash the US$ Index taking it to lows of 70.81 by March 2008.

So what next? The US$ Index has broken out of what appears as a large symmetrical triangle bottom pattern. The pattern suggests a move for the US$ Index to a minimum objective of 106. The US$ Index is quite extended at this time so a period of consolidation and correction could soon get underway. This may not be much different from corrective periods seen in 1981 during the 1980-1985 period and in 1998 during the 1995-2001 period. The current rally had its beginnings with a low in May 2011. Given that the two previous periods saw the US$ Index rise for 5/6 years the current rise for the US$ may be half way through its up move in terms of time.

There are as noted similarities between the current period of a rising US$ Index and the two previous periods. The most notable is the potential negative impact on US exports and the massive amount of US$ debt assumed by emerging markets. Since the collapse of Bretton Woods, the end of the gold standard in 1971 and the onset of floating exchange rates the world has gone through a series of sharp ups and downs for the US$, currency crises (Mexico, Asian currency crisis, Russian financial crisis, Argentina crisis) and a series of financial/banking crises (1973-1975, 1980-1982, 1987-1990, 2000-2002 and 2007-2009).

A characteristic of each crisis is that it took increasing amounts of debt to “buy” ones way out of the crisis. Since the 2008 financial crisis, the world has added some $57 trillion in debt according to a recent study by McKinsey & Co. Of the total $25 trillion has come from governments. But $7 trillion has been added by households, $18 trillion by corporations and $12 trillion by financial institutions. Corporations in both Canada and the US are sitting on large amounts of cash and have been criticized by government for not investing the cash in the economy. Given extremely low interest rates for savers including negative interest rates in some instances (Switzerland, Denmark) there are signs that savers are hoarding cash. Retail participation in the stock markets is at one of its lowest levels ever. All of these are signs of deflation.

A favourite cry of many is the expression “this time is different”, that somehow all the current instability in currencies and the massive debt exposure (and don’t forget the $600 trillion in derivatives that is tied to the debt and currencies) is somehow normal and as long as the stock market keeps going up what does it matter. In the end, however, financial history has shown that it is not different. Only the players change.

Copyright 2015 All rights reserved David Chapman

General Disclosures

The information and opinions contained in this report were prepared by Industrial Alliance Securities Inc. (‘IA Securities’). IA Securities is subsidiary of Industrial Alliance Insurance and Financial Services Inc. (‘Industrial Alliance’). Industrial Alliance is a TSX Exchange listed company and as such, IA Securities is an affiliate of Industrial Alliance. The opinions, estimates and projections contained in this report are those of IA Securities as of the date of this report and are subject to change without notice. IA Securities endeavours to ensure that the contents have been compiled or derived from sources that we believe to be reliable and contain information and opinions that are accurate and complete. However, IA Securities makes no representations or warranty, express or implied, in respect thereof, takes no responsibility for any errors and omissions contained herein and accepts no liability whatsoever for any loss arising from any use of, or reliance on, this report or its contents. Information may be available to IA Securities that is not reflected in this report. This report is not to be construed as an offer or solicitation to buy or sell any security. The reader should not rely solely on this report in evaluating whether or not to buy or sell securities of the subject company.

Definitions

“Technical Strategist” means any partner, director, officer, employee or agent of IA Securities who is held out to the public as a strategist or whose responsibilities to IA Securities include the preparation of any written technical market report for distribution to clients or prospective clients of IA Securities which does not include a recommendation with respect to a security.

“Technical Market Report” means any written or electronic communication that IA Securities has distributed or will distribute to its clients or the general public, which contains an strategist’s comments concerning current market technical indicators.

Conflicts of Interest

The technical strategist and or associates who prepared this report are compensated based upon (among other factors) the overall profitability of IA Securities, which may include the profitability of investment banking and related services. In the normal course of its business, IA Securities may provide financial advisory services for issuers. IA Securities will include any further issuer related disclosures as needed.

Technical Strategists Certification

Each IA Securities technical strategist whose name appears on the front page of this technical market report hereby certifies that (i) the opinions expressed in the technical market report accurately reflect the technical strategist’s personal views about the marketplace and are the subject of this report and all strategies mentioned in this report that are covered by such technical strategist and (ii) no part of the technical strategist’s compensation was, is, or will be directly or indirectly, related to the specific views expressed by such technical strategies in this report.

Technical Strategists Trading

IA Securities permits technical strategists to own and trade in the securities and or the derivatives of the sectors discussed herein.

Dissemination of Reports

IA Securities uses its best efforts to disseminate its technical market reports to all clients who are entitled to receive the firm’s technical market reports, contemporaneously on a timely and effective basis in electronic form, via fax or mail. Selected technical market reports may also be posted on the IA Securities website and davidchapman.com.

For Canadian Residents: This report has been approved by IA Securities, which accepts responsibility for this report and its dissemination in Canada. Canadian clients wishing to effect transactions should do so through a qualified salesperson of IA Securities in their particular jurisdiction where their IA is licensed.

For US Residents: This report is not intended for distribution in the United States.

Intellectual Property Notice

The materials contained herein are protected by copyright, trademark and other forms of proprietary rights and are owned or controlled by IA Securities or the party credited as the provider of the information.

Regulatory

IA Securities is a member of the Canadian Investor Protection Fund (‘CIPF’) and the Investment Industry Regulatory Organization of Canada (‘IIROC’).

Copyright

All rights reserved. All material presented in this document may not be reproduced in whole or in part, or further published or distributed or referred to in any manner whatsoever, nor may the information, opinions or conclusions contained in it be referred to without in each case the prior express written consent of IA Securities Inc.

More from Silver Phoenix 500