S&P500 In The Aftermath Of Fed’s $2.3Trillion Backstop

Let’s join yesterday’s Gold & Silver Weekend Special, and bring you an advance one in stocks as well. As the coronavirus crisis, response and anticipations are what is moving the markets, today’s Alert will draw on yesterday’s Gold & Silver Trading Alert and offer additional thoughts as relates to stocks.

Despite the technologically advanced world we live in, this opening statement holds particularly true:

(…) The observation is that the real numbers and the reported numbers might not be the same thing. In fact, it's neither likely, or even possible that they are equal.

First of all, it's really difficult to assess if someone died from Covid-19 or something else, if they were not tested before they died and too much time passed since their death to know if it was from Covid-19 or something else. The symptoms are similar to other illnesses, so it's particularly difficult. Moreover, if someone had some sort of pre-existing illnesses or conditions, it's difficult to say if their death is due to Covid-19 or that condition. The definitions of what should be counted as a Covid-19 death and what not can also vary.

The above comes on top of whether someone dies because of the virus, or while having it in their system. Prevalence, frequency and reliability of testing is a factor – and none of this has been, is or will be at the same standard throughout the geographies impacted, let alone throughout the US.

By the way, the testing itself isn’t a settled subject. Apart from the issue of continuing availability of testing reagents, is it really 2019-nCov that is coming up as positive? And what about the swab tests’ reliability in general – are those negatives really negatives? Quite a lot appears to be slipping through the cracks undiagnosed – and definitely not only in Massachusetts.

The health status, demographics, population density and lifestyle – these are among the leading determinants of the virus progression. And so is the policy response, as we’ll mention further on.

You might ask, why the focus on the deaths? Arguably, they’re the easiest ones to track (accounting for the above limitations). But in a way, they’re a lagging indicator as equal focus should be also on R0 (showing how fast the infection spreads person-to-person) and testing prevalence (it’s not just availability but also repeat, as in repeated testing).

All these metrics show how the flatten-the-curve efforts work. And the lockdowns certainly buy some time and do work in this aspect. But how will the people take to them over time, and how to set their expectations in light of this crisis? The below quote takes on the dilemma:

(…) let's assume that you're the one leading the nation, and you want to somehow deal with the situation. If you do too little, millions will die and you will be blamed, and if you do too much, bring soldiers to the streets etc. you risk massive riots, perhaps open fights, protests, or even a civil war. What do you want people and the economy to do?

Of course, you want the economy to get back on its track as soon as possible, but you can't risk the virus getting out of hand, due to the above. So, what do you do? You want to make sure people are scared exactly as they should be scared - not more, not less. People have to be scared to obey the lockdown and prevent the virus from spreading. However, if they are too scared, nobody will go to work - not even those who are now called "essential". Ultimately the economy would grind to a halt, and the people would get out on the streets, rioting anyway.

There you have both the incentive and legitimate desire to get the economy going as soon as you can. Other considerations are:

- the stress and damage to the supply chains

- consumer confidence and lifestyle habits

- small and medium business capacity to absorb the shocks

- the ability to buy time and soften the blow via monetary and fiscal interventions

This is an election year, and the longer it all drags on, the harder it’ll be to recover economically. Trump is in an unenviable position of making the call (on moving) to reopen the economy. Will he go the technocratic route that Canada or Australia appear to be taking? Waiting for some vaccine that’s supposed to be safe, instead of UK’s call to get back to work because people will be exposed to the virus no matter what? Sweden hasn’t gone the route of strict restrictions, and aims for its people to develop natural immunity instead. Striking the balance right is ultimately what Trump’s reelection hinges on.

A few more thoughts on vaccines. Please note the development of never before used DNA and mRNA vaccines that change the DNA structure both within the individual, and potentially mankind – will the coronavirus vaccines be their debut? This goes well beyond the risk of immune system going into overdrive, triggering a cytokine storm. One can’t help but remember the Louis Pasteur vs. Antoine Bechamp completely different view on infectious diseases that can be for brevity’s purposes summarized as “The microbe is nothing, the terrain is everything.” Towards the end of his life, Pasteur admitted to his germ theory being wrong as the milieu is everything. In other words, that’s a point for “Treat the patient, not the infection”, and against the germ phobia.

In this light, focus on the two-week window of public’s attention makes perfect sense in managing the fallout:

(...) It has been only two weeks since widespread pandemic lockdowns were implemented in the US and as expected the public is not handling the idea very well. Within one week there were already frantic demands for the economy to reopen by Easter (spurred on by Donald Trump), and mass delusions have developed that this is still going to happen despite the fact that lockdown guidelines have been extended to at least April 30th. People desperately want to believe that this will all be over in a matter of weeks.

Many governments continue to perpetuate this fantasy by using very carefully worded terminology. For example, the phrase “two weeks of hell” is being consistently repeated by the media after Trump uttered the notion a few days ago. In Italy, a Milan official sees lockdowns now continuing for 2-3 more weeks. In Spain, the public was left with the impression that two solid weeks of quarantine and lockdowns would help stave off infections, yet the government extended the restrictions for…yes, you guessed it…another two weeks.

Why are these announcements always in two week intervals? I suspect it is because this the maximum amount of days before the average person begins to register the passage of time in their minds in a new situation. After two to three weeks of going without certain comforts and habits, people tend to adapt and find different ways of doing things. And, after two to three weeks of crisis, they might wake up and recognize the situation is not going to get better.

Governments and establishment elites are seeking to keep the public as passive and docile as possible by continually feeding them the notion that the worst of the pandemic will be over in a matter of weeks. And, every two weeks they will reassure us that we are “only two weeks away” from salvation.

Sure, the rate of the death toll’s rise will be decreasing. Before diving into the price paid, let’s mention some more on the issue of reported deaths:

(…) Let's recall what the official death toll prediction from the White House was.

It was between 100k and 240k Americans.

Let's also recall how much the data was underreported in case of the swine flu (H1N1) - 15 times. The data was underreported 15 times and it was generally accepted by the world without negative consequences to anyone. "Oh well, estimation mistakes happen, carry on..."

Combining both gives us the situation in which it might be a reasonable decision to tell people that the likely death toll is about 15x smaller than the really realistic expectation. It was already done, so it should have no negative consequences when it turns out that the numbers were way off. At the same time, it gives people hope, as this number - while big - is considerably smaller than the cancer death toll for example. It doesn't look extreme - it looks bad but rather relatively "normal".

Remember our estimation of the US death toll for Covid-19 at about 2M Americans? Well, if we divide it by 15, we'll get... about 133k Americans. Let's reverse the order. Multiplying the official prediction by the factor of 15, we get 1.5M - 3.6M Americans.

This could be White House's realistic expectation of the total Covid-19 death toll, while the 100k - 240k was what they found to be optimal to report.

Please note that the White House declined to provide the explanation behind this prediction. Obviously "you know, we took the real estimation and divided it by the biggest number we know that we can easily get away with" is not an acceptable explanation. Of course, we are not making any accusations here, just speculating on what might have or might have not been the case...

Let’s dive into our four considerations in reopening the economy:

- the stress and damage to the supply chains – it’s not only high-tech, industrial or medical production lines that have been hit. Food supply, agriculture comes right next as it depends on workforce availability. Undoing the benefits of international division of labor would result in reduced supply and higher cost base, and jumpstarting it is no small feat.

- consumer confidence and lifestyle habits – Thursday’s University of Michigan preliminary consumer sentiment reading of 71 not only came well below expectations, but marked a 9-year low. That's likely just a beginning of the darkening prospects. As the real economy stands and falls with the consumer, how fast confidence is regained and life moves back towards normal, will determine the recovery from this fall of a Seneca-like cliff. Former Fed Chair Janet Yellen warns of a 30% Q2 2020 GDP drop, which coupled with the unprecedented job losses reaching many new millions on a weekly basis, is a virtual guarantee of tough times ahead. Do you think that Americans have just enough emergency savings aside to weather the storm? Many don’t, as the survey showed that 60% won’t be able to cover basic financial needs with even less than a month-long quarantine. What does that mean for housing? Foreclosures, evictions and a crisis in its own right.

- small and medium business capacity to absorb the shocks – don’t take for granted that whatever business was closed, will just spring to life back as soon as the restrictions are lifted. As China’s experience shows, not only are existing businesses closing down, but new ones aren’t coming into existence quite as fast either. With an average US small and medium enterprise having cash flow for around two months’ on hand, and providing for the majority of US employment – what will the upcoming data show? Don’t wave it off with Thursday’s $2.3T Fed loans promise, as taking even an interest-free loan is a sizable risk given the lockdown lifting and consumer habits return uncertainty. Even if we see an initial V-shaped recovery in demand, what else would you expect from people confined to their homes with the exception of grocery shopping or medical visits, as soon as the restrictions are lifted? With all the fear embedded, how are sport stadiums, concert venues, movies or the whole leisure and hospitality sector going to cope? The stock market seems too optimistic about the return to pre-corona status quo in our opinion, and the jury is still out as to whether we would get a U- , L-, or even W-shaped recovery instead.

- the ability to buy time and soften the blow via monetary and fiscal interventions – the Fed has certainly been doing all it can to soften the blow and kept the monetary spigots open. Buying hand over fist so many asset classes in sight, it has calmed the panic, and certainly appears to be winning this fight at the moment. So did China’s Shanghai Composite when their markets reopened after the Lunar New Year. The Fed’s avalanche of money and backstops shows up in the debt markets’ performance, pushing this massive deflationary event into the background for now. Yes, coronavirus means destruction on both the demand and supply sides. A new equilibrium will emerge, and it will be quite different from the previous one. While the deflationary forces take time to run their course, the policy response can (temporarily, until the bond vigilantes show up – or have they died out?) stun and overwhelm the markets. And that’s what we’re seeing in stocks currently. Sure, the just-offered loans to keep the payrolls running, are forgivable, but they come with their own string of attachments – stock buybacks (financial engineering being one of the engines of the stock bull market), is history now. How much time before dividends are questioned – what shape will it leave the retirees and pension funds in as we remain stuck in a yield-starved environment that’s pushing everyone farther out on the risk curve? How will earnings projections take to the coming downgrades – downgrades both in future earnings and creditworthiness in general? As they say, the bond guys get it right more often that the stock market participants, let’s check several charts (charts courtesy of http://stockcharts.com) now.

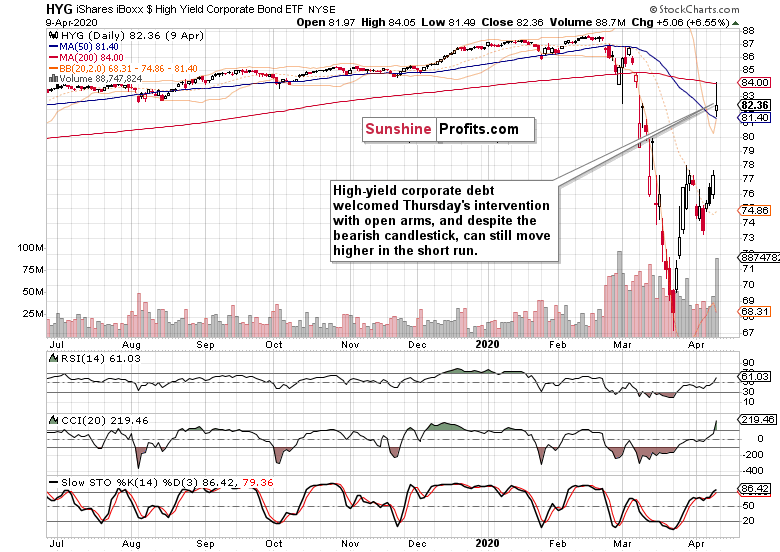

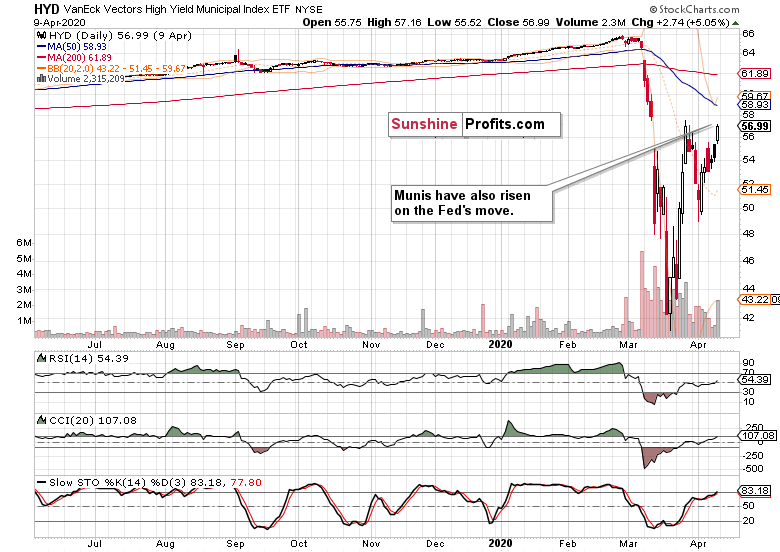

Starting off with the debt market ETFs, we see that:

Both high-yield corporate debt and municipal bond moved up, as the Fed’s support has broadened in scope. And as Treasuries (yes, even long-dated ones – not only the short-term ones such as SHY) remained relatively stable, the spreads with these riskier counterparts have narrowed. This points to improving financial system conditions, and is a leading and positive short-term indicator for stocks.

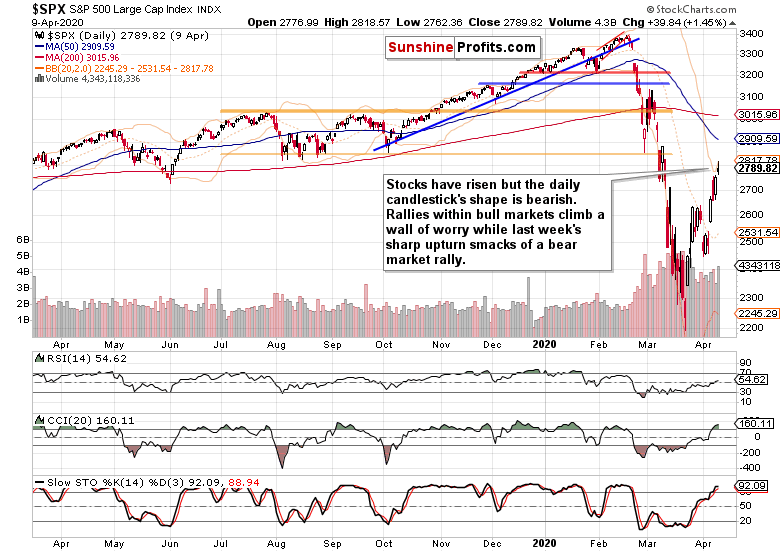

Let’s check Thursday’s S&P 500 (SPY ETF) performance next.

Stocks didn’t really have any other option but to gap at the open on such a Fed announcement. But the bulls had trouble extending gains considerably, which brought us that bearish candlestick.

The week which just ended, brought us quite a sharp rally - Wile-e-Coyote style. Such a steep pace is what usually punctures periods of declines within bear markets, and isn’t really consistent with the historic experience within bull markets.

These were our Thursday’s observations in the latest intraday follow-up:

(…) On one hand, the Fed’s aggressive move made it clear that we have a Powell put now – they won’t hesitate to throw money in clever ways at the economic contraction. Today’s trading action so far shows that the markets are unwilling to fight the Fed, and low volatility attests to that.

On the other hand, the coronavirus situation appears still far from being resolved. The curve isn’t flat yet but the markets are merrily disregarding it for now. Stocks and debt welcome papering the effects over currently.

The time of questioning the Fed regardless of the resolve of policy steps taken, will come. And so will the deterioration in the coronavirus situation and grappling with the economic aftermath. Out of the four considerations mentioned above, the Fed can exert control only over the fourth one.

Let’s quote from yesterday’s Gold & Silver Weekend Special as regards stocks:

(…) It means that the US stock market (and other stock markets) are likely to fall further and the huge stimulus is unlikely to prevent it. The only thing that it is likely to do is to delay the slide.

The stock market is likely slide based on the fear triggered by the increasing death toll, but that’s not all that people will consider while determining whether to sell or buy stocks. They will also pay attention to how long will the quarantine take place, as it severely limits the economic activity. And it will remain in place for much longer than a few weeks.

(…) "I want to get it open as soon as possible," Mr Trump said at a Good Friday briefing at the White House. "I would say without question it's the biggest decision I've ever had to make."

However, no action would be taken until the government knew the "country [was] going to be healthy", he said. "We don't want to go back and start doing it over again.”

(…) There’s almost zero chance that the US economy will be fully re-opened by the end of April, and quite many people appear to believe that it’s very likely… Which explains why the rally in the stock market did not end yet.

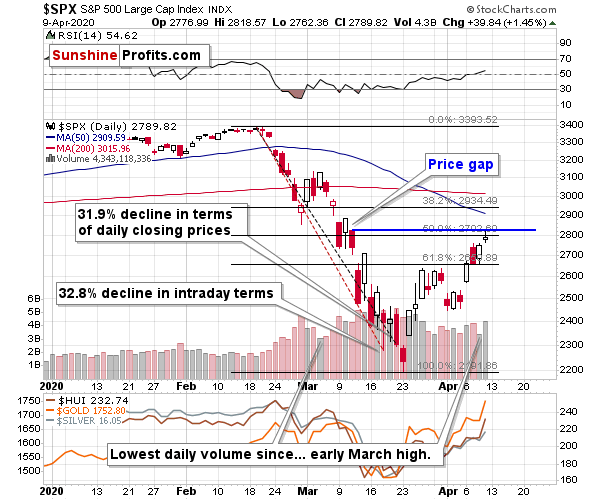

Actually, it might have just ended on Friday, as stocks were up by just 1.45% despite another massive wave of stimulus from the Fed, which is a very weak reaction.

The S&P 500 managed to move to the lower border of the mid-March price gap and temporarily (!) move above the 50% Fibonacci retracement based on the February - March decline. This breakout was invalidated before the end of the day. The doji candlestick that formed on relatively big volume (biggest in April) doesn’t mean much, but if stocks open lower on the next trading day and decline during the day, the last three candlesticks will create an “evening star” candlestick pattern (based on these three sessions), which is one of the rarer, but also one of the most reliable bearish (reversal) signs. Of course, stocks would have to decline…

That’s another piece arguing for the case that stocks will have to grapple with tough times ahead. The incoming data for April and May will be particularly soft, from consumer confidence, manufacturing, unemployment or GDP, you name it.

Summing up, the bulls seized the short-term momentum, and a short-term bottom looks very likely to be in. Despite the upswing though, stocks aren't out of the woods just yet. While bidding their time, the sellers are highly likely to become active at the nearest opportunity, which however doesn't appear to be immediately at hand. The bulls took advantage of Thursday’s Fed support, and the short-term momentum appears to be on their side for now. The medium-term outlook however remains bearish, and the short position is therefore justified going into Monday’s session.

We encourage you to sign up for our daily newsletter - it's free and if you don't like it, you can unsubscribe with just 2 clicks. If you sign up today, you'll also get 7 days of free access to our premium daily Stock Trading Alerts as well as our other Alerts. Sign up for the free newsletter today!

Monica Kingsley

Stock Trading Strategist

Sunshine Profits - Effective Investments through Diligence and Care

* * * * *

All essays, research and information found above represent analyses and opinions of Przemyslaw Radomski, CFA and Sunshine Profits' associates only. As such, it may prove wrong and be subject to change without notice. Opinions and analyses were based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are believed to be accurate, Przemyslaw Radomski, CFA and his associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Mr. Radomski is not a Registered Securities Advisor. By reading Przemyslaw Radomski's, CFA reports you fully agree that he will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Przemyslaw Radomski, CFA, Sunshine Profits' employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

********

Monica Kingsley is a trader and financial markets analyst. Checking dozens of charts daily, she integrates their messages with economics and in-depth experience. Trade calls and writing are her cup of tea as much as studies in market histories. Having been at the financial markets when the Great Recession arrived, she experienced many bull and bear markets - be it in stocks, bonds, gold and silver. https://www.monicakingsley.co

More from Silver Phoenix 500