Two Steps Forward, One Step Backward in the S&P500, Right?

Stocks defended the opening bullish gap, and scored further gains intraday before the sellers took over in the session's final 45 minutes. Have we seen a turning point?

In short, that's unlikely, and let me tell you why exactly I think so.

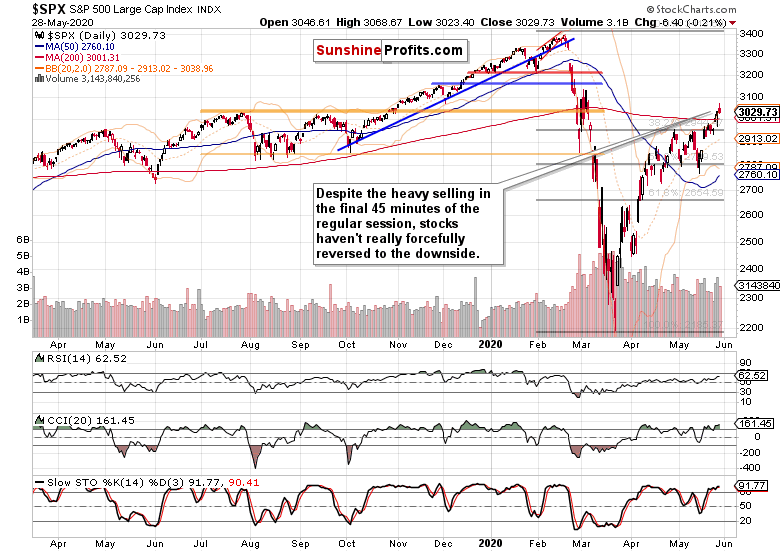

S&P500 in the Short-Run

Let’s start with the daily chart perspective (charts courtesy of http://stockcharts.com ):

The day looked like the bulls were firmly holding the reins, but another daily setback struck as we approached the closing bell. I say daily, because the volume didn't really overcome its recent highs, and stock prices haven't suffered a profound setback either. All that the bears were able to achieve, was pretty much reminiscent of the stock behavior during the unfolding breakout above the 61.8% Fibonacci Retracement..

In other words, yesterday's setback isn't really a fly in the ointment for the bulls. The daily indicators keep supporting the bulls, with no imminent sell signals. The sky still remains clear for the buyers for now.

Yesterday’s Alert captures the key reason why:

(…) Against the backdrop of strengthening high yield corporate bonds (HYG ETF), the S&P 500 upswing has been progressing nicely throughout the day, and a local top in either seems to be very far away indeed.

While the sellers might try to close the week and month on a bearish note, the above words ring true also today because we haven't seen junk corporate bonds falling through the floor. Let's see precisely what I mean by that.

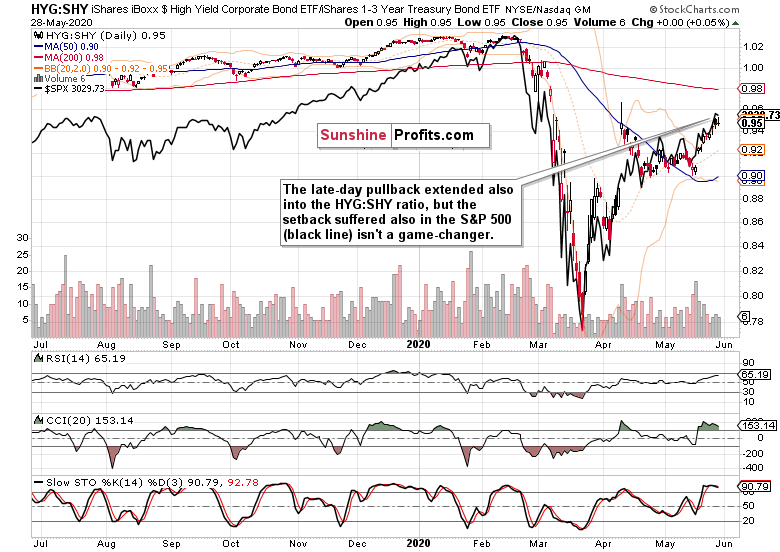

The Credit Markets’ Point of View

High yield corporate bonds (HYG ETF) gave up all their gains since the market open, but the relatively low volume of the daily upswing rejection continues to favor the bulls. While it wouldn't come as a surprise to see a sharper consolidation of recent sharp gains, a running consolidation with higher highs and higher lows is all we've been getting so far. And that's a very bullish type of consolidation, boding well for the credit markets.

In short, the credit market uptrend is well established, and serves as a tailwind for stocks.

The chart of the high yield corporate bonds to short-term Treasuries ratio (HYG:SHY) with the overlaid S&P500 prices (black line), also supports the view we haven't seen a game-changer yesterday.

Key S&P 500 Sectors and Ratios in Focus

While technology (XLK ETF) gave up its intraday gains, the swing structure of higher highs and higher lows, remains intact. And that's the definition of what an uptrend is. The sector simply appears to be trading sideways, consolidating recent sharp gains. Yesterday's lower volume versus the preceding higher one, sends a bullish message as buyers appear in droves when prices get lower.

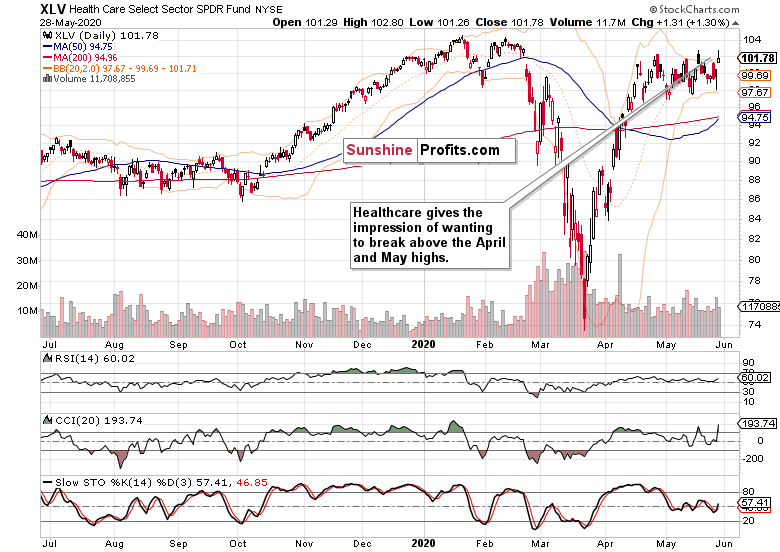

Just as the tech sector, healthcare (XLV ETF) also supports the prospect of more gains to come. It's been knocking on the door of April and May highs, and an upside breakout of the recent trading range is only a matter of time in my opinion.

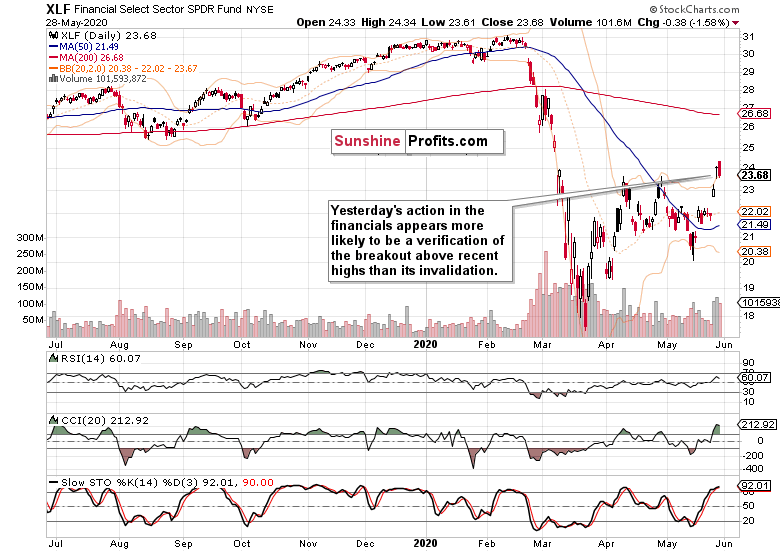

The price action in the financials (XLF ETF) also follows a bullish path. We've seen volume rise during last three sessions, and yesterday's session gives an impression of verification of the breakout above the April highs as the sector is consolidating recent gains.

The volume differential that favors the bulls is even more pronounced in the consumer discretionaries (XLY ETF). Real estate (XLRE ETF) for example, just extended its recent gains yesterday, disregarding the move lower in the index.

It has been only the leading ratios that suffered pronounced setbacks yesterday, as consumer discretionaries to staples (XLY:XLP) challenged their Wednesday's intraday lows, and financials to utilities (XLF:XLU) moved below them already. But we haven't seen what mathematicians would call an inflection point yet. In other words, it's likely we'll see both ratios stabilize and support the move higher in stocks next.

As for the stealth bull market trio, materials (XLB ETF) outperformed both energy (XLE ETF) and industrials (XLI ETF) as the latter two closed down – but again, on lower volume than during the preceding up days. Overall, this bull market trio still favors the stock upswing to continue.

Summary

Summing up, yesterday’s late-day reversal didn’t likely mark a call to start selling lock, stock and barrel everything in sight. Conversely, it appears to be a part of the ongoing consolidation that keeps resulting in higher highs and higher lows. As today is the last trading day of the week and month, the closing prices are of key importance for the timing of the anticipated challenge of the early March highs. While the credit market and sectoral analysis favor the stock upswing to continue, yesterday's weak performance of the Russell 2000 (IWM ETF) is a short-term watchout. The balance of risks is skewed to the upside over the coming weeks though.

I expect stocks to slowly grind higher overall despite the high likelihood of sideways-to-slightly-down trading over the summer – but we’re nowhere near the start thereof. Right now, the breakout above the three key resistances (the 61.8% Fibonacci retracement, the upper border of the early March gap, and the 200-day moving average) is still unfolding with the bears running for cover and FOMO (fear of missing out) back in vogue. In short, the ball remains in the bulls’ court to show us what they're made of. Will the weekly and monthly closing prices later today still lean in the bulls' favor on higher timeframes? I would cautiously say so.

Last but not least, we'll hear Powell speak later today, and Trump will focus on China. When the latter has been announced, it marked the start of the heavy S&P 500 selling 45 minutes before the closing bell yesterday. As tensions have been rising, the short-term direction in stocks very much depends on the overall balance of President's announcement as regards Hong Kong, the Uyghur bill, coronavirus, the China-India border and foremost the trade deal. We'll monitor and act accordingly on the unfolding developments.

We encourage you to sign up for our daily newsletter - it's free and if you don't like it, you can unsubscribe with just 2 clicks. If you sign up today, you'll also get 7 days of free access to our premium daily Stock Trading Alerts as well as our other Alerts. Sign up for the free newsletter today!

Monica Kingsley

Stock Trading Strategist

Sunshine Profits: Analysis. Care. Profits.

* * * * *

All essays, research and information found above represent analyses and opinions of Monica Kingsley and Sunshine Profits' associates only. As such, it may prove wrong and be subject to change without notice. Opinions and analyses were based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are believed to be accurate, Monica Kingsley and her associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Ms. Kingsley is not a Registered Securities Advisor. By reading Monica Kingsley’s reports you fully agree that he will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Monica Kingsley, Sunshine Profits' employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

*********

Monica Kingsley is a trader and financial markets analyst. Checking dozens of charts daily, she integrates their messages with economics and in-depth experience. Trade calls and writing are her cup of tea as much as studies in market histories. Having been at the financial markets when the Great Recession arrived, she experienced many bull and bear markets - be it in stocks, bonds, gold and silver. https://www.monicakingsley.co

More from Silver Phoenix 500