UK Election: Ignores BREXIT, GREXIT And Real Economic Risks

- UK election today expected to yield “hung parliament”

- Election not seen marked decline in pound as was the case in run up to last election

- Election ‘chaos’ could trigger a ‘Lehman moment’ for pound

- Recent history shows Labour victory not inherently bad for sterling

- Concern that Miliband’s Labour closer to that of Brown than Blair

- BOE warn deficits could “trigger a deterioration in market sentiment towards the UK”

- “Punch and Judy” politics ignores BREXIT, GREXIT and significant economic risk

People across Britain are going to the polls today to elect a new government. Opinion polls suggest that, as in 2010, a hung parliament is likely as neither the Tories nor Labour are likely to gain an overall majority.

The uncertainty caused by a hung parliament has historically had a negative impact on markets and on the pound as investors wait for clarity in government policy before making investment decisions. There is also the possibility of more serious market dislocations and concerns that election ‘chaos’ could trigger a ‘Lehman moment’ for the pound.

We think it is important to look at short term dynamics and long term ones.

Dominic Frisby, the precious metal and financial markets commentator at Moneyweek, has written an interesting article in which he looks at how the election result may impact the pound in the short term.

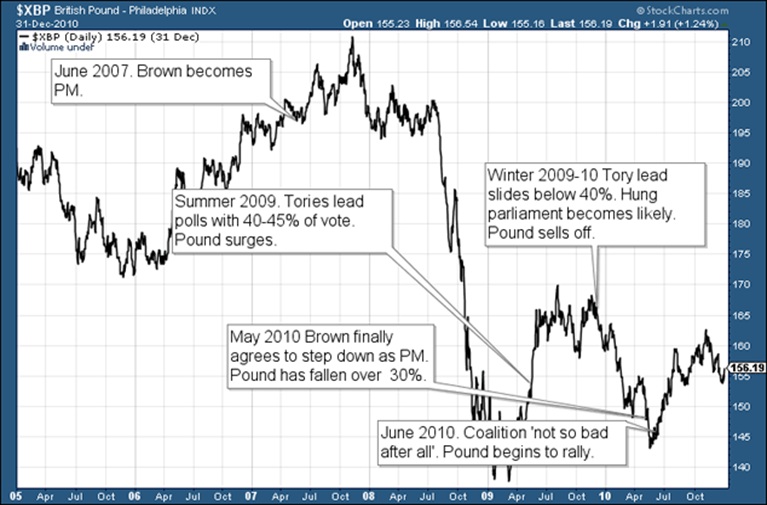

He comments on how well sterling is bearing up despite the widely anticipated hung parliament. Back in 2010 in the two weeks prior to the election, when it was becoming clear that a hung parliament was the likely outcome, sterling fell from $1.55 to $1.47. Even after the Cameron-Clegg coalition was announces the pound continued to fall bottoming out at $1.43.

By contrast, since the beginning of this year, despite election jitters and uncertainty regarding Britain’s future, the pound is down only 4 cents against a strong dollar and up 7 cents against the euro.

It would seem that foreign exchange traders are not as daunted by the prospect of a hung parliament knowing the track record of the current coalition. They expect the Conservatives and Lib-Dems to again form the new government.

Frisby has speculated that a Labour-led government would, at least initially, have a negative impact on sentiment towards the pound.

He points out that it does not necessarily follow that accession of a Labour government implies a weaker pound. Under Blair’s tenure the pound rose from $1.59 to $2.

However, Miliband’s Labour are regarded as being closer in nature to that of Gordon Brown than the Labour of Tony Blair. The pound fared very poorly under Brown’s tenure. Following an initial surge to $2.10, it crashed over the next few years to below the $1.40 mark. In fairness, this was against the backdrop of a stronger dollar and the global financial crisis.

The decline was only reversed in April 2009 when opinion polls showed the Tories having 40% of the vote. And when that figured slipped below 40% the pound also began to slide again.

Traders of sterling prefer the Tories as they are seen as more fiscally responsible than the “tax and spend” Labour party . Frisby concludes that a conservative led government would be met with “a sigh of relief”. He adds that a Miliband government may do a good job but it will need to earn the confidence of foreign exchange traders and initial reactions would be negative.

There is, of course, many a slip ’tween the cup and the lip. If voters return an unexpected result – and the balance of power held by the various players is significantly different from that which is expected – uncertainty would come surging back into the system.

This would likely cause considerable volatility in the foreign exchange markets and could see sterling come under pressure.

Dominic’s piece was very much focussed on the short term ramifications of the election outcome on sterling. Were he to consider the bigger picture and the longer term issues, we believe Dominic would voice concerns about sterling in the coming years and share our view that sterling will again come under pressure and depreciate particularly against gold in the coming years.

The fact that the election barely touched on the very poor fiscal position of the UK does not bode well for sterling in the long term.

Gold in GBP – 10 Years

The UK’s twin budget and current account deficits remain stubbornly high despite the recent recovery and measure around 5 per cent of gross domestic product (GDP).

Interestingly, the Bank of England has said on the eve of the election that the UK current account deficit, which measures the gap between money flowing out of the UK and money brought in, was “large.” The BoE warned that if the economy deteriorated, it could “trigger a deterioration in market sentiment towards the United Kingdom.”

This poses a threat to the economy in the event of the UK economy or global economy slowing down. Other real risks to the UK being ignored for now are the increasing threat of Scottish independence and of BREXIT should the Tories be reelected.

Meanwhile, GREXIT remains forgotten for now but a Greek default and contagion in the eurozone would impact on the UK gilt market and indeed the global bond bubble. This would in turn badly affect the vulnerable, debt-laden UK economy.

It is amazing the economic ‘elephants in the room’ that can be ignored by “Punch and Judy” political pundits and politicians.

Politics in the UK and internationally has been reduced to a soap opera involving faux debates between so called left wing and right wing parties that rarely address the real challenges facing us all today. It also involves politicians making promises they cannot keep or will not keep.

Sadly, the UK electoral debate about the economy has fitted this bill and almost wholly ignored the real global economic, financial and monetary challenges facing the world today.

The politicians like the bankers and the central bankers, are happy to kick the can down the road and let their successors and future generations pick up the tab and pay for the economic mess that they refuse to address.

Deep down we all know that not addressing unpleasant economic realities can only go on for so long.

Breaking News and Research Here

MARKET UPDATE

Today’s AM LBMA Gold Price was USD 1,183.00, EUR 1039.840 and GBP 776.94 per ounce.

Yesterday’s AM LBMA Gold Price was USD 1,191.25, EUR 1,063.41 and GBP 785.22 per ounce.

Gold in U.S. Dollars – 1 Week

Gold and silver saw small price gains yesterday of 0.1 and 0.24 per cent to $1,191.970 and $16.50per ounce respectively.

In Asia overnight, Singapore gold prices ticked lower and have flat lined in London trading this morning.

World financial markets were unsettled again today as a week-long sell-off in ‘safe haven’ government bonds, stocks and the dollar and a sharp rally in oil prices showed little sign of relenting.

Nerves were still jangling in Europe and shares and bonds got off to another poor start on fears the recent surge in bond yields, the euro and energy costs could snuff out the only recently-formed hopes of a solid eurozone recovery.

British 10 year gilt yields hit their highest level since November as part of a further wave of heavy sales of sovereign debt on international markets today.

********

Courtesy of http://www.goldcore.com/us

Mark O'Byrne is executive and research director of www.GoldCore.com which he founded in 2003. GoldCore have become one of the leading gold brokers in the world and have over 4,000 clients in over 40 countries and with over $200 million in assets under management and storage.We offer mass affluent, HNW, UHNW and institutional investors including family offices, gold, silver, platinum and palladium bullion in London, Zurich, Singapore, Hong Kong, Dubai and Perth.

Mark O'Byrne is executive and research director of www.GoldCore.com which he founded in 2003. GoldCore have become one of the leading gold brokers in the world and have over 4,000 clients in over 40 countries and with over $200 million in assets under management and storage.We offer mass affluent, HNW, UHNW and institutional investors including family offices, gold, silver, platinum and palladium bullion in London, Zurich, Singapore, Hong Kong, Dubai and Perth.

More from Silver Phoenix 500