Was That An S&P500 Reversal? Most Probably Not!

Despite opening with another bullish gap, the buyers just could push stocks higher yesterday. But the futures have rebounded in the overnight trading, so can the S&P500 upswing continue now?

Let’s check yesterday’s developments on the daily chart (charts courtesy of http://stockcharts.com ).

S&P 500 in the Short-Run

Yesterday’s red candle shows the reversal of fortunes. The key question is whether it’s a short-term, one-day phenomenon, or whether it marks a local top.

Volume would slightly lean in favor of the bears, but the daily indicators haven’t suffered much with yesterday’s downswing. Preceding price action supports upswing continuation – after all, we have made neither a lower high, nor a lower low.

As a result, the benefit of short-term doubt still goes to the bulls. With prices back above the 50% Fibonacci Retracement, it’s up to them to show us they can make it to the 61.8% Fibonacci retracement next, and close the early March bearish gap in the process.

Let’s dive into the reasons why we think the upswing has a pretty good chance of continuing.

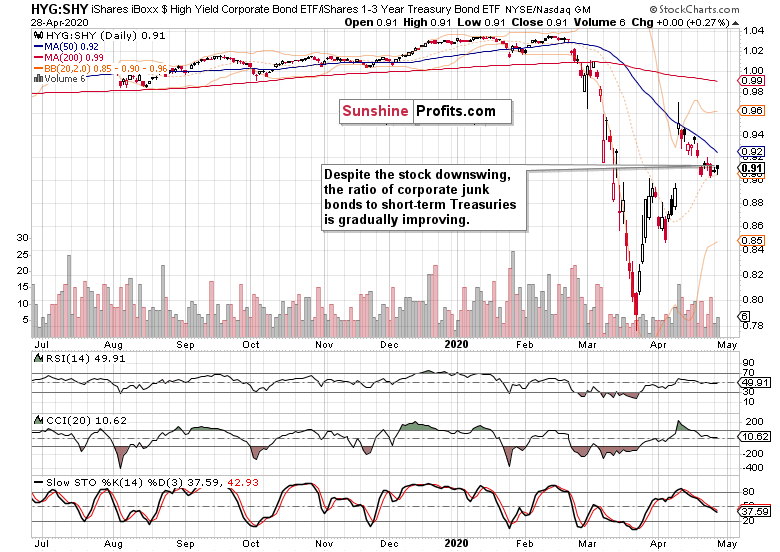

The Credit Markets’ Point of View

Credit markets are a key ingredient in stock analysis. Does the riskier corner (well, considering the breadth of the Fed intervention, what is actually the riskiest one now?) of the debt instruments support stocks going higher?

Just as high yield corporate bonds (HYG ETF) themselves, their ratio to short-term Treasuries (SHY ETF) kept more than steady yesterday. That’s an encouraging sign pointing to the stock market recovery being not too far behind. In other words, yesterday’s setback is likely a short-term phenomenon only.

How did yesterday’s S&P500 decline reflect upon its key sectors?

Key S&P500 Sectors in Focus

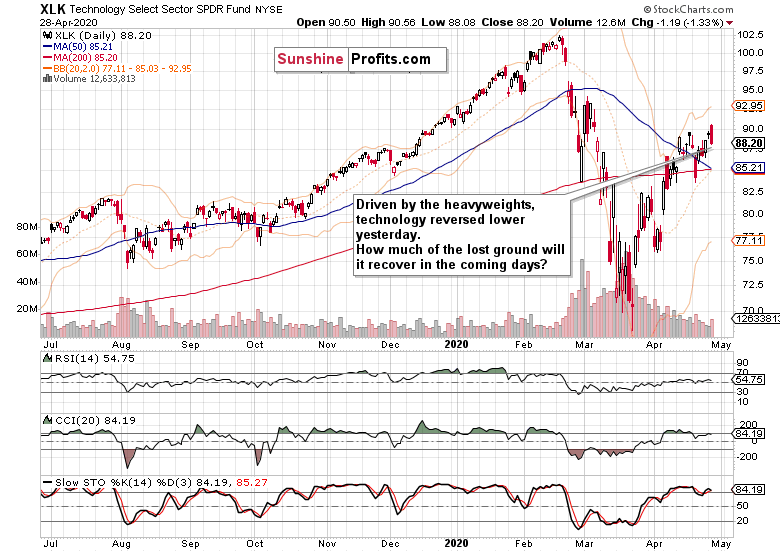

There’s no denying that technology reversed yesterday, led by the heavyweights. As Alphabet (GOOG) was about to release its earnings after the market close, the uncertainties-driven downswing is understandable. But the disappointment wasn’t really there to the degree feared. Yes, ad sales slowed down but revenue climbed 13% as the net income has scored merely a 1.5% gain. This illustrates that the ad market downturn is starting to cut into profitability.

The upcoming quarter will be hard on advertising. Being as diversified as Alphabet is though, the company will weather the storm. Its shares liked the earnings conference call message, and reacted with an upswing in aftermarket trading.

This bodes well for the other tech behemoths such as Amazon (AMZN), Microsoft (MSFT), Apple (AAPL) or even Intel (INTC) as they report. And as a result, for the tech sector as such.

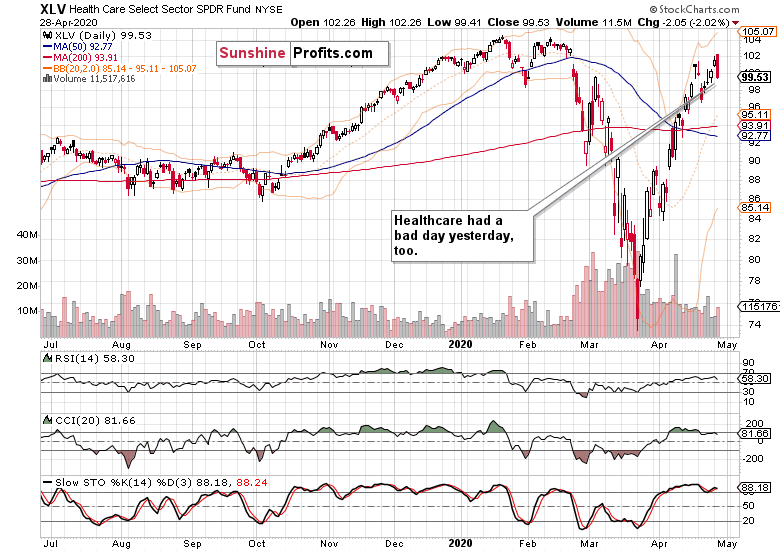

Healthcare was the other sector leading yesterday’s S&P 500 downswing. It also happened on sizable volume, and the extended daily indicators have taken a hit. Considering the sharpness and momentum of the recovery from the Mar 23 lows, it wouldn’t be unimaginable to see the sector taking a breather and consolidate over the coming sessions.

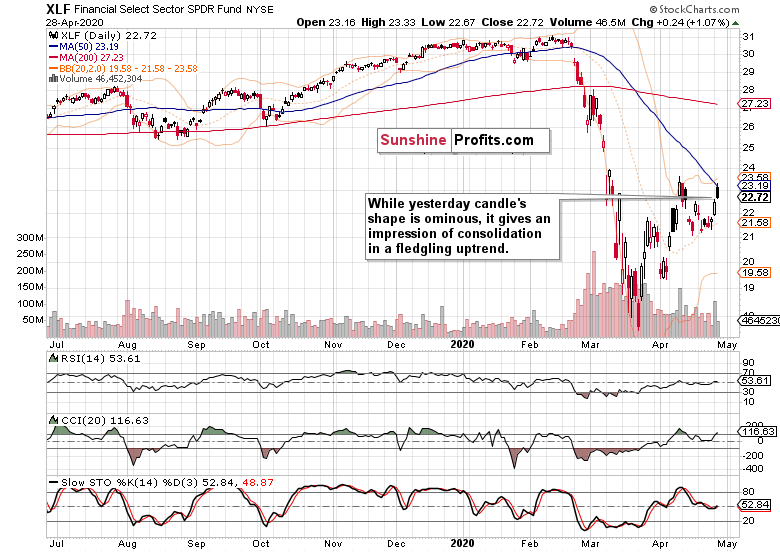

Which sectors would then help drive the index upswing? Despite the lackluster oil performance, energy (XLE ETF) and materials (XLB ETF) with industrials (XLI ETF) not lagging behind, are the places to look at. And among the S&P 500 sectoral heavy-weights, financials (XLF ETF) are doing quite well too.

Let’s quote our yesterday’s observations:

(...) Our Friday’s takeaway was that financials don’t appear to be willing to decline much further these days and that the odds favor their next move to be up. And in line with anticipation and the signals from the credit markets, they’ve indeed turned steeply higher yesterday. This development bodes well for the risk-on assets and further index gains.

Even accounting for yesterday’s downswing, they still closed the day higher than on Monday. Coupled with the discussed resilience in credit markets, this bodes well for the upcoming strong showing of the sector.

Please note the low volume of yesterday’s session – it doesn’t point in the direction of us having seen a reversal yesterday. The daily indicators haven’t suffered much either, and looking at the premarket S&P500 upswing (futures are trading back around 2885 currently), it’s more than likely that financials will finish up today.

The Fundamental S&P 500 Outlook

Later today, the Fed will announce its new monetary policy decisions, and of course hold a press conference. These were our yesterday’s thoughts:

(…) Do the markets expect a new move out of this meeting? Yesterday, Bank of Japan took some more action, whetting the appetite around the world. But will the Fed deliver in a meaningful way? Probably not, as we look rather to the wait-and-see attitude to win overall at this meeting with perhaps a few bones thrown here and there.

Should the Fed meeting outcome be largely along these lines, stocks waver thereafter. But the tape tells us that the expectations are for the Fed to have the bulls’ back.

These points remain valid. We’ll monitor the unfolding news and market reactions in real-time, and issue an intraday Stock Trading Alert to discuss the breaking developments and our moves.

Summary

Summing up, even accounting for yesterday’s downswing, S&P 500 trades solidly above the 50% Fibonacci retracement, and remains primed for further gains. Among the key sectors, technology and healthcare were hardest hit, while financials held up fine and the stealth bull market trio (energy, materials and industrials) continued to perform. The key ratios (financials to utilities, and especially discretionaries to staples) haven’t really suffered a profound setback yesterday either. More than a cursory examination of yesterday’s Alphabet earnings report also supports the case for the tech sector moving higher later today. The balance of risks remains skewed to the upside and our profitable long position remains justified.

We encourage you to sign up for our daily newsletter - it's free and if you don't like it, you can unsubscribe with just 2 clicks. If you sign up today, you'll also get 7 days of free access to our premium daily Stock Trading Alerts as well as our other Alerts. Sign up for the free newsletter today!

Monica Kingsley

Stock Trading Strategist

Sunshine Profits - Effective Investments through Diligence and Care

* * * * *

All essays, research and information found above represent analyses and opinions of Przemyslaw Radomski, CFA and Sunshine Profits' associates only. As such, it may prove wrong and be subject to change without notice. Opinions and analyses were based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are believed to be accurate, Przemyslaw Radomski, CFA and his associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Mr. Radomski is not a Registered Securities Advisor. By reading Przemyslaw Radomski's, CFA reports you fully agree that he will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Przemyslaw Radomski, CFA, Sunshine Profits' employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

********

Monica Kingsley is a trader and financial markets analyst. Checking dozens of charts daily, she integrates their messages with economics and in-depth experience. Trade calls and writing are her cup of tea as much as studies in market histories. Having been at the financial markets when the Great Recession arrived, she experienced many bull and bear markets - be it in stocks, bonds, gold and silver. https://www.monicakingsley.co