A Permabear's Dilemma As Market Top Draws Near

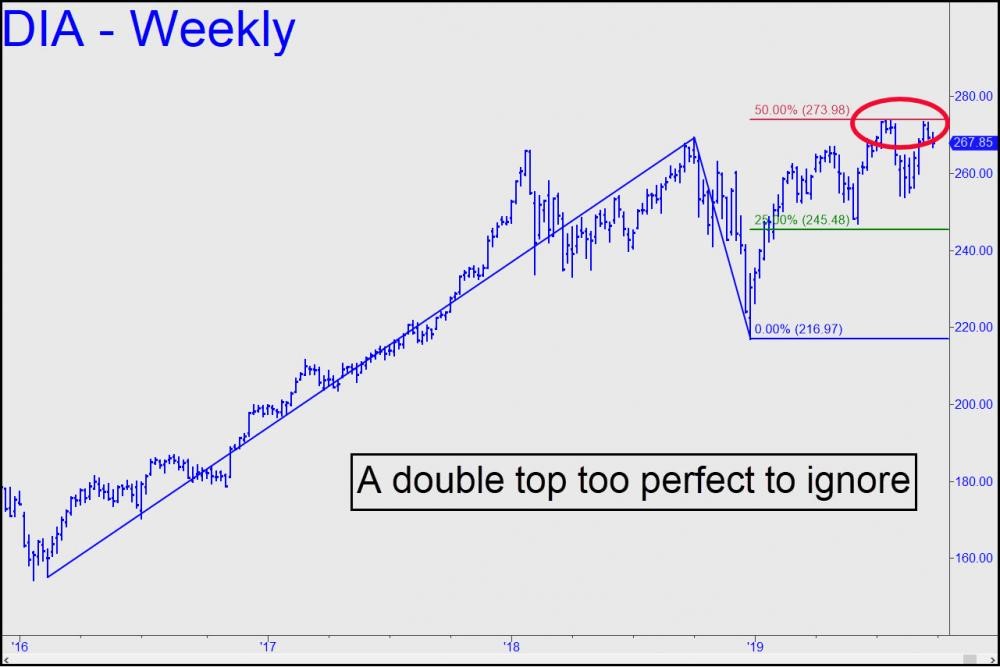

Readers rightfully took me to task last week for putting out two headlines that appeared to at least mildly contradict one other and which taken together could only have left one wanting more clarity. The first said Don’t Load Up on Puts Quite Yet; the second, There’s Still Time to Load Up on Puts. So which is it? Do we get short here, or not? Well, the answer, like the market itself, is more art than science and for me reduces to this: The bull’s ten-year rampage has at least a little farther to go, but it can’t hurt to nibble on put options now, just in case. Thus was your editor a buyer of DIA October 4 265 put options on Friday after pondering the chart above. It is one that I’d shared with you earlier but which I put aside in favor of an AAPL chart that looked more bullish. It still does, and it leaves me quite confident that shares of Apple, a key bellwether for the bull market, are very likely to rise from a current 219 to at least 242 before the fat lady sings. That would equate to a rally of about 10 percent, which, if it occurs, would imply that the broad averages will remain buoyant at least until then.

Formidable Wall of Worry

Like many of you, I’m convinced stocks are a bad risk at these levels. Indeed, it is not difficult to reel off a list of good reasons why a bear market should already have begun. September is historically the market’s worst month, and this year there were plenty of things to worry about when it commenced. For one, Europe is well into a recession that threatens to be bottomless. At the same time, China’s growth has contracted sharply. The trade war has dramatically slowed the global economy and smothered capital investment everywhere. U.S. manufacturing output has begun to drop, accompanied recently by a steep plunge in consumer confidence. Of even greater concern is that consumer spending itself, the main engine of U.S. prosperity, has started to weaken. Unsold automobiles from 2019 are piling up on the lots and the crucial housing sector is in an apparent dead-cat bounce, spurred by desperate Fed maneuvering. The central bank is struggling increasingly to hold a potentially catastrophic deflation at bay, unable to prop up even crude oil’s price. Sobriety has returned to the IPO market with a vengeance, forcing WeWork’s greedy handlers to abort a deal tied to a $50 billion valuation when it got marked down to $15-billion-or-less. Perhaps most significantly of all, the corporate money freed up by Trump’s tax cuts has been spent after having pumped almost two trillion dollars into share buybacks over the last two years.

Party Is Over

On the evidence, only an idiot could doubt the party is over. And yet, U.S. stocks have been frolicking in record territory since early July, detached not only from such concerns, but from reality. In the meantime, trying to predict exactly when a decade of easy-money madness will end is a fool’s errand. Despite this, for most professional forecasters the challenge is too tempting to pass up. Gurus have technical tools that supposedly can help us put this nearly impossible feat within reach. In truth, we are no better at it than you and possess no special knowledge that would give us an edge. Like you, and considering the recessionary drift of the global economy, we regard the stock market at these levels as nothing short of terrifying. A few hundred dollars invested in put options from time to time is not likely to produce big profits, if any, but it can help one sleep a little easier.

********

More from Silver Phoenix 500