QE Is Over And Is Not Working! Interest Rates Will Continue Higher As Risk Is Coming To The Fore. (Part 1)

QE is over in the Eurozone! Risk is being reflected in the interest rates, finally! And it looks like the monetary authorities are pretending economic strength, for political reasons, possibly justifying an interest rate hike.

The authorities are showing “strong” economic figures because they don’t have any option. They have been trying to build confidence in the economy by throwing money from the helicopters without sorting any real effect but for creating bubbles in the equity, bond and housing markets. And now they have to keep that story up despite adverse economic figures because that would defeat all the stimulus efforts. So they need to pretend the economy is strong (hence why there are so many divergent opinions within the Fed) and thus therefore need to increase interest rates. It is a credibility issue. San Francisco Fed President John Williams said on Tuesday May 12 that he wants the U.S. central bank to start raising rates "a bit earlier" so that the path of rates can be gradual. This suggests that a rate hike in June is not out of the question. Waiting until "we're face-to-face with 2% inflation" isn't a wise course because the Fed might have to engineer a more dramatic rate hike which could upset markets and damage the economy, Williams said in a speech to the New York Association for Business Economics. Though when the Fed increases interest rates, which might be sooner than a lot of people expect (because they can’t admit failure) the weak economy will implode and the real, unbiased facts will surface!! Just look at the April retail figures (no rebound despite a so-called severe winter!! excuses, excuses and excuses by everybody interviewed on CNBC).

I think that in recent weeks a shift has taken place, we have finally arrived at the point that risk, stemming from a potential Grexit, the weak economic fundamentals, the threat of a rate hike and the central banks losing credibility, is being reflected in the bond yields. We have entered the danger zone! According to an article in Bloomberg more than $450 billion has been wiped out across global bond markets in the past few weeks. With the high leverage this figure is most likely much higher. QE doesn’t work any longer in my point of view and rates can’t be pushed down much further anymore. And any remark by Draghi like “whatever it takes” will most likely embarrass him greatly. By the way don’t forget he was co-chairman of Goldman Sachs in Europe when Goldman’s “helped” Greece with creative accounting getting the country into the Eurozone! We are in the last phases of this casino world. Even Steve Wynn is complaining about the weakness in the economy and he has a pretty good “betting” record!

The more bonds the central banks buy the fewer bonds will be available in the “free” market for long term bonds and thus even more illiquidity will ensue pushing interest rates up even further when profit taking sets in. Next to that it should be noted the Chinese are not buying as many bonds anymore, they need the money for their own economy.

You can’t spend yourself out of debt; we have seen it in the US, Japan and now China and the Eurozone. In the last couple of weeks we have witnessed that the ECB can’t push interest rates further down in negative territory. The ECB and central banks got egg on their face. One of the catalysts for the bund’s plunge was a weak French OAT auction, which saw yields rise and bid/cover ratios decline at 2023 and 2025 bond actions. "The big fallout in core fixed income occurred after a very soft French auction with a large tail which collapsed the market again." In other words very, very weak. Though everything is interrelated hence the fallout of the German bunds and US treasuries and other government bonds. We witness a worldwide trend of higher rates and a lower dollar.

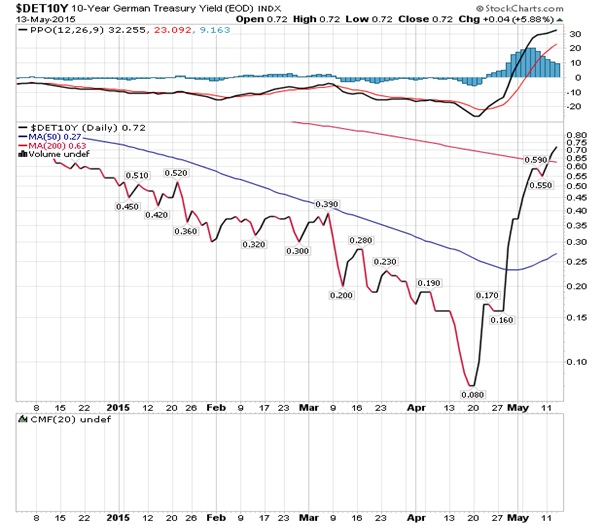

The bund holders voted with their feet and took profits on their hugely inflated bund prices, and swapped recurring income for capital gains, hence the sharp rise in rates from 0.05 bps on April 17th to 0.80 bps on Thursday May 7th with the German 10yr yield breaking above its 200 daily moving average of 0.635%. On May 13 the bund yield closed at a high for the day of 0.73% after having seen a low of 0.60%.

The Treasury market also sold off again in tandem with the bunds on Tuesday morning May 12, pushing the yield on the benchmark 10-year Treasury up 8 basis points to a high of 2.36%, the highest point since Nov.21. The next day the 10-year Treasury fell to 2.29% though closed again higher for the day at 2.29%. Investors are clearly selling into strength with the Fed intervening. The intense selling in the Treasury market was fueled by the meltdown in the Eurozone's government bond market, which has been going on for more than two weeks powered by risk, finally reflected in interest rates. As factors behind the selloff are mentioned: (1) negative interest rates (capital gains), (2) a bad French auction, (3) a potential Grexit, (4) the weak economic fundamentals (GDP, inventories, retail sales), (5) stronger commodity futures, (6) the threat of a rate hike (credibility) and (7) the central banks losing credibility (when is QE is not working, weak retail sales, it starts to undermine the currency). Another important factor for higher rates might be the fact that (8) the Chinese are buying less and less bunds and treasuries because they need the money for their own economy. China has debts of approximately $28trn!

China's foreign currency reserves had their biggest quarterly drop US$113 billion on record in the first three months of the year and the Yuan is trading at the closest to fair value since 2010, according to Goldman Sachs. That means less demand for assets in Dollars and Euros from the world's biggest creditor. The Chinese central bank has amassed US$3.73 trillion in currency reserves over the past decade in a bid to hold down the value of the Yuan and underpin the competitiveness of its exporters. As the government in Beijing changes gear, needing to fund the transformation from an export led economy to a consumer led economy cultivating domestic demand to sustain economic growth, it may affect European bond markets just as much as the Greek efforts to win better terms from creditors. In other words there will be fewer and fewer funds available from China for foreign bonds.

With the scarcity in the bond markets, there are not enough government bonds available in the “free float” and thus I can’t see how the ECB can push interest rates down again. And we should look at this especially in the context of the increasing illiquidity that is plaguing these markets. The Eurozone government-bond market is some €11 trillion whilst the Eurozone’s corporate market is some €5trn and the ECB and central banks are buying some €60bn government and private sector bonds a month till September 2016 or €1.1trn in total or some 7% of the total outstanding Eurozone government and corporate bonds. The purchases started in March and are intended to run through to September 2016. Mr. Draghi signaled the purchases could extend further if the ECB isn’t meeting its inflation target of just below 2%. But the more bonds the central banks buy the less long-term bonds will be available in the “free” market and thus even more illiquidity will ensue as a result of the cornering of the bond markets by the CBs. And as such the central banks are pushing interest rates up themselves even further when investors take profits and cash in capital gains. Anyway QE seems to be over in my point of view, they have failed.

Will Yellen do “a Greenspan”, pretending the economy is performing better than it really is, and create a 2002-2005 upheaval in the bond markets? She probably will for “credibility” reasons.

The ten million dollar question is if these higher rates are a blip or a trend change. Comparisons have been made with the GJB yields between 2002-2005, which showed similar initial behavior. The extremely low yielding Japanese bonds suddenly saw their bond market collapse when Greenspan cut US rates less than expected following pressure of the White House to give a more rosier picture of the US economy, pretending that the US economy was stronger than it really was for political purposes, heard before? Within hours, Greenspan's comments triggered the biggest massacre on the bond market since the Long-Term Capital Management collapse in autumn 1998.

Chart: Bloomberg

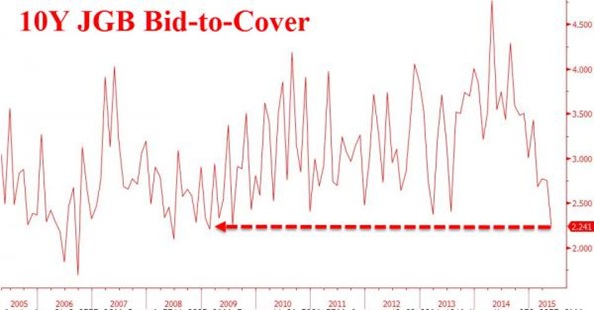

On May 12 we just witnessed the Japanese 10Y JGB auction to report the lowest bid-to-cover ratio since Feb 2009 at just 2.24x with a notable tail of 1.1bps (the widest since March) as it appears once again, the total dissolution of liquidity from the second largest bond market in the world has left the BoJ and Ministry of Finance losing control. According to some people a 100bp interest rate shock (see chart here above) in the JGB yield curve, would cause a loss of ¥10tr or $83bn for Japan's banks!

Despite the unrest in the global bond markets Yellen might still feel “forced” (for political, credibility and “confidence boosting” reasons) to increase interest rates to keep the idea high that the economy is really improving! Next to that she also said "I would highlight that equity market valuations at this point generally are quite high. There are potential dangers there." Yes there are potential dangers here but they have been solely created by the central banks themselves!!!! And you can imagine how this would all “NOT” work out this time. Why? Because the stretch in the system is finished and investors will soon find out how weak the economy is!

A lot of indicators are showing a weak economy, well that is if you, unlike Wall Street, are willing to see the facts.

We just saw that first quarter GDP growth was a paltry 0.2% GDP following the $126 billion increase in inventories otherwise GDP would have been a whopping negative 2.6%. On May 13 the Atlanta Fed cut its Q2 GDP forecast once more, this time to 0.7% from 0.8%. On top of that that major retailers are closing some 6,000 locations over the next 18 months because the forecast are so good! U.S. retail sales for April came in unchanged from March, when a 0.2% rise was expected. The retail sales report is one of the most important U.S. economic data points of the month. The U.S. dollar index slumped on the news and is hovering near a four-month low at 93.60 whilst gold is up $25/oz. The 90 level looks clearly in sight, see chart below.

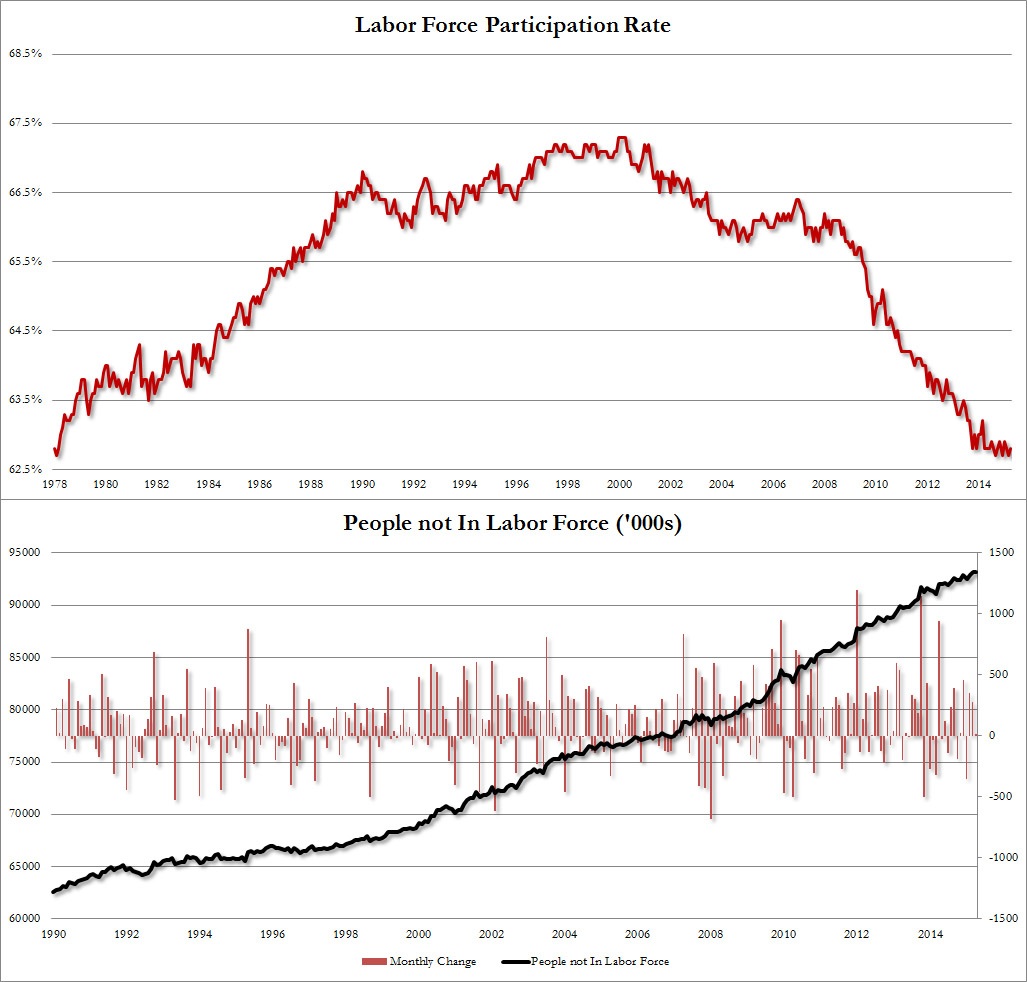

The weakness in the economy is obvious for people who want to see it. If you don’t want to see it because your income depends on it (Wall Street) you don’t, it is as simple as that. Though ultimately you can only fool everybody for so long. With the BLS figures being BS as some people are arguing, the “Birth/Death Model” assumed that 213,000 jobs were created by anticipated (fictive) new businesses out of a total of a 223,000 published non-farm payrolls for April. On this basis only 10,000 real jobs were created. Another fact that the US economy by far is not as strong as is being suggested. ADP Payroll reported 169,000 new jobs for April. And if you believe that the unemployment rate is only 5.4% also look at the 93.1 million of the working age population that is not considered to be part of the labor force. The number of Americans not in the labor force rose once again, this time to 93,194,000 from 93,175,000, with the result being a participation rate of 69.45% or just above the lowest percentage since 1977. This is strong evidence of an economy slowing. Do you need any more news?

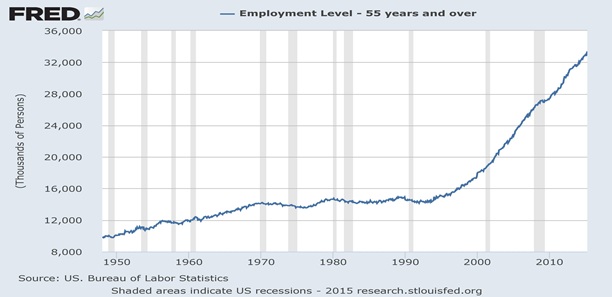

As mentioned before when we analyze the employment figures we should also look at the low quality new jobs created and the fact that the 55-year and older make up an ever-larger part of the employed workforce because their pensions don’t suffice because their pensions have been destroyed by Greenspan and Bernanke.

The chart below shows how America is slowly but surely transforming from a manufacturing society to one of waiters and bartenders (no added value). Perhaps a better way to show the transformation is the following: since the start of the second great recession in December 2007, there have been 1.4 million manufacturing jobs lost. They have been almost completely "offset" by the 1.3 million waiter and bartender jobs gained. Manufacturing has been replaced by service in other words less and less is being manufactured in the US!

Huge disconnect between price action in physical markets where differentials are signaling oversupply and futures markets where all looks rosy. Sounds familiar with respect to what has been going on for so long in the precious metal markets!

Barclays is warning investors with respect to the commodities. According to the Barclays report it will prove very tough to make further significant gains in commodity prices from here unless supply/demand conditions improve very fast. There are a multitude of factors but what troubles them the most is the huge disconnect between price action in physical markets where differentials are signaling oversupply and futures markets where all looks rosy. Energy markets, especially oil, look most exposed and although copper fundamentals are firmer and prices less at risk of a large downward adjustment, volatility is likely there too, especially if further weakness in China becomes more evident (see chart below). The risks for a reversal in recent commodity price trends are growing, and with fewer market makers to absorb the shocks, potentially, a period of high volatility could lie ahead.

In my opinion either some investors are anticipating too much recovery in particularly oil or copper and want to profit from the low prices or some “other” forces are manipulating the futures markets in order to pretend that there is much more strength in the economy than there really is hence the weakness in the physical. Remember paper futures can easily be used to influence prices whilst the physical always is the real deal! And the Chinese industrial production figures as shown in the chart below are not particularly signaling strong demand for copper. Copper often is referred to as the benchmark for the health of the economy. You draw your conclusion how China is faring these days.

In my point of view there are 2 contrarian forces working: 1 – The Governments that want to pretend that the economy is improving, is doing better (higher commodity prices, higher interest rates) 2 – Fundamentals that clearly indicate that conditions are not rosy at all.

Amongst the abovementioned factors the commodity price rally has been an important influence on the recent pickup in global bond yields. Although these yields remain low versus historical levels some of the recent action has been eye-catching and it is hard to imagine that the moves would have been quite as aggressive without the French auction gone bad, profits from negative interest rates and the big move up in commodities, particularly oil. See the chart below showing the correlation of the higher interest and the higher oil prices.

The ultra-low or negative rates could only be sustained for so long. Paying interest to the borrower is in direct violation with the principle of charging interest for using the money, for the opportunity costs and for the risk involved of not getting your money back. Investors clearly preferred to lock in their capital gains.

Anyway whatever the reason it looks like bonds are still not cheap here and clearly some nervousness is likely to continue. It looks like people want to get rid of their bonds before everybody is going for the gates and finds out that there are no bids and that the stop losses don’t work!

© Gijsbert Groenewegen, May 14, 2015

********

More from Silver Phoenix 500